Growing Again From a New Starting Point

The United States is more than a year removed from the official end of the recession, according to the National Bureau of Economic Research. Yet, the most common question on the lips of business leaders seems to be, “Really?” After 20 years of the most stunning economic growth and technological advancement in human history, the definition of what normal growth is may have changed. Current projections for real GDP growth are between 2 and 3 percent for much of the immediate future.

Economies around the world have strengthened to a point where a double-dip recession is increasingly unlikely, but a slow rate of growth seems unavoidable. Many of the key reasons for recent growth, both real (introduction of computers, the Internet) and artificial (credit bubbles), have either run their course or been removed from the market entirely. Technological advancements will always continue to increase productivity, but the boost seen in the last two decades may not be duplicated for a long time to come, and that will lead to less immediate growth.

“Looking at the economy on a global level, we are out of the woods, but we still have a long way to go,” says Tony McKinnon, president of MRINetwork. “The natural rate of growth for companies over the next five years isn’t going to be what we experienced before the recession. Success is going to be hard earned, and even more of that success will be driven by the performance of impact players than ever before.”

For evidence of the slow, but steady state of the recovery, one needs to look no further than private employment levels. The top line number—total U.S. non-farm employment—has bounced up and down wildly in recent months. This volatility has been the result of both temporary census positions coming then going, combined with large local government layoffs. Yet, private employment has settled into a slow, steady rate of growth.

In August, on a seasonally unadjusted basis, private employment was up year-over-year for the first time since early 2008 and the first months of the recession. In economic terms, the labor market has established a new equilibrium from which it can grow, and this is the general trend being seen across the economic indicators.

Two years of low labor liquidity first caused job openings to dry up, then uncertainty caused candidates to question the safety of changing positions. Mixed with the job dissatisfaction a recession naturally causes, today’s passive candidate market may be as rich as it has been in years.

News/Insights

Job Market/Industry News

Job Market/Industry News

The Power of Emotional Intelligence in the Doctor-Patient Relationship

Jun 5, 2023

“Physician leaders who are able to exhibit high degrees of emotional intelligence (EI), particularly in how they manage their own emotions and react to the emotions of other...

Hiring

Hiring

Where Are All the Dentists?

Oct 27, 2021

The market for dental talent has always been competitive. Several factors have combined to make what was already a tight market even more challenging. These include: Grad...

Job Market/Industry News

Job Market/Industry News

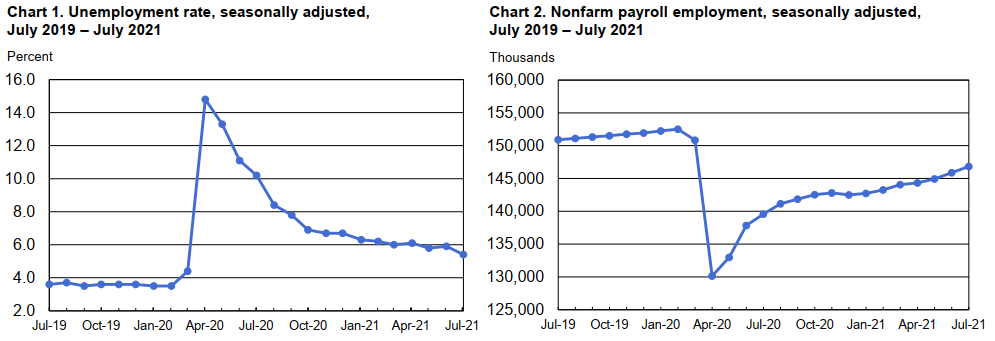

Employment Situation Report – July 2021

Aug 9, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report For the seventh straight month, the U.S. Bureau of Labor Statistics (BLS) reported a significant...

Job Market/Industry News

Job Market/Industry News

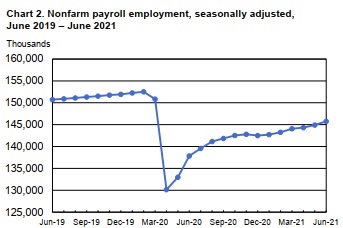

Employment Situation Report – June 2021

Jul 2, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report – June 2021 Continuing a six month increase in job growth, the U.S. Bureau of Labor Statisti...

Job Market/Industry News

Job Market/Industry News

Employment Situation Report – May 2021

Jun 4, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report – April 2021 The U.S. Bureau of Labor Statistics (BLS) today reported total nonfarm payroll ...

Job Market/Industry News

Employment Situation Report – April 2021

May 7, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report - April 2021 The U.S. Bureau of Labor Statistics (BLS) today reported total nonfarm payroll em...

Job Market/Industry News

Employment Situation Report – March 2021

Apr 5, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report The U.S. Bureau of Labor Statistics (BLS) today reported total nonfarm payroll employment incr...

Hiring

Hiring

Are You Ready for What’s Next?

Mar 24, 2021

Everyone is trying to understand what’s coming next in a post-COVID-19 world. While we have no special foresight into the future of the pandemic, we can tell you what we hav...

Job Market/Industry News

Employment Situation Report – February 2021

Mar 9, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report The U.S. Bureau of Labor Statistics (BLS) today reported total nonfarm payroll employment increa...

Job Market/Industry News

Employment Situation Report – January 2021

Feb 10, 2021

Summary of the Bureau of Labor Statistics Monthly Employment Situation Report The January job gain of 49,000 was in-line with most analysts’ expectations and represented an...